The markets rebounded on Monday after President Trump said that discussions with Iran about ending the war were going well. As a result, the S&P 500, NASDAQ Composite, and the Dow were all up more than 1% on the day, with the Russell 2000 jumping 2.3%.

There's a good chance that this won't last, but you've got to take what you can get in these volatile markets.

Among Barchart’s top 100 bullish price surprises from yesterday, a tiny, micro-cap building materials stock caught my eye.

Virginia-based Smith Midland (SMID) has a market cap of $159 million. Its share price jumped 14% on Monday on minimal volume. Its standard deviation was 2.58, the 21st-highest on the day.

Normally, I wouldn’t bother with a stock this small, but when I took a closer look at the business—my wife runs a small construction company, so I’m always interested in related businesses—and who its largest shareholder is, I just had to write about it.

The Business

Although it’s only a micro-cap, Smith Midland’s been around since 1960. Founded by David G. Smith on the family farm, it began life as Smith-Cattleguard, the name being a nod to its original product, a precast concrete cattleguard to prevent cows from wandering onto other farms in the area.

And so, a focus on precast concrete was born. 10 years after its launch, the company moved off the farm and into a new 10,000-square-foot plant. Smith Midland’s been there ever since. It changed its name to Smith Midland in 1985.

Today, it has several patented and proprietary products according to its 2024 10-K:

1) SlenderWall, a patented, lightweight, energy-efficient concrete and steel exterior wall panel for use in building construction;

2) J-J Hooks, a patented precast concrete highway safety barrier;

3) SoftSound, a proprietary sound absorption finish that’s used on sound barriers to absorb traffic noise;

4) Sierra Wall, a patented sound barrier for roadside use; and

5) Easi-Set and Easi-Span patented transportable concrete buildings.

In addition to these five products, Smith Midland continues to make cattleguards and other precast products from three facilities: Midland, Virginia (the original), Reidsville, North Carolina, and Hopkins, South Carolina.

Several Revenue Streams

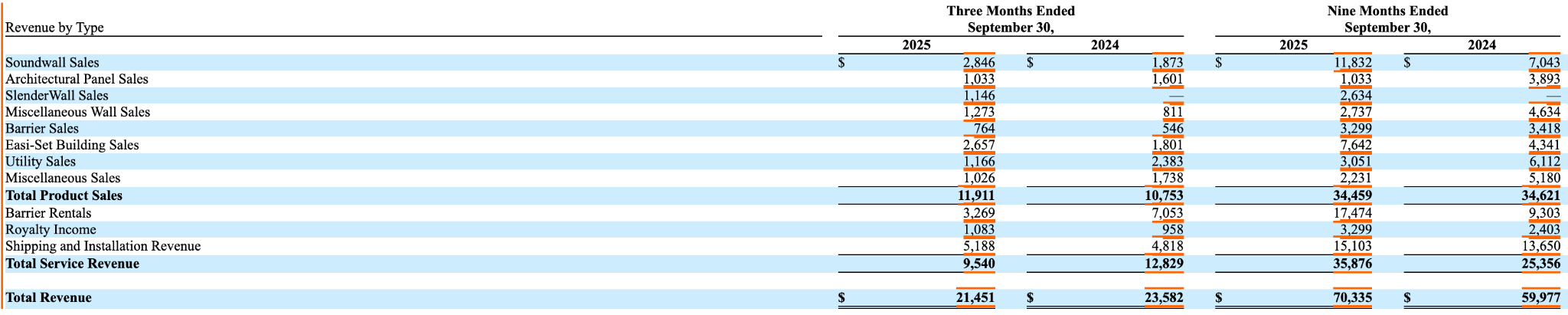

In 2024, the company generated 58% of its $78.5 million in revenue from product sales and the remaining 42% from service revenue. That’s a nice balance.

Drilling down further, it has four revenue streams: product sales (49% of revenue), barrier rentals (25%), royalty income (5%), and shipping and installation (21%). That’s also a nice balance.

Based on preliminary Q4 2025 results, it expects 2025 revenue to be $93 million at the midpoint of its guidance, 18.5% higher than $78.5 million in 2024. In addition to the highest annual revenue in its history, the company expects record net income for the year.

Through the first nine months of 2025, three things jump out.

First, its Soundwall sales are up 68% year over year. Secondly, it has SlenderWall projects in 2025; it did not in 2024; and lastly, its Barrier rentals saw an 88% increase in sales through Sept. 30, 2025.

The benefit of higher service revenues -- they increased by 41% over the same nine months, which includes barrier rentals -- is that they have higher margins than product sales, boosting profitability.

The Largest Shareholder

Let’s face it, Smith Midland isn’t a sexy business. It will never hold a candle to Palantir (PLTR) or other AI stocks. However, it makes real things that we need in our lives. Infrastructure-focused products that won’t go away with AI. Combined with a long history in the precast concrete market, it’s proven it has the staying power to still be in business a decade or two from now.

That’s a good thing.

The largest shareholder is Thompson Davis & Co., a Richmond, Virginia-based investment adviser. As of Dec. 31, 2025, it owned 34.58% of Smith Midland. Its investment accounted for nearly 40% of the $167 million reported in its Q4 2025 13F.

The second-largest investment was a $9.2 million position in Carlisle Companies (CSL), a manufacturer and supplier of roofing and other construction products. Makes sense given the financial adviser specializes in the research of industrial companies such as Smith Midland and Carlisle.

Thompson Davis first acquired shares in Smith Midland (966,080) in Q4 2021. It has added to its holdings over the past four years, nearly doubling its position. It understands the building materials industry. Further, it is located within two hours of Smith Midland, which helps.

Smith Midland went public in December 1995, selling one million shares at $3.50 each. At the time, its revenues were $10 million. Its revenues and share price have both increased at a compound annual growth rate of nearly 8%.

It’s not massive growth, but over 30 years, the gains add up.

Why Buy SMID?

I think this stock is for investors who like diamonds in the rough. It’s a business that can continue to exist for as long as it wants. It’s growing at a sustainable rate, it has a healthy balance sheet, and it plays in an industry that’s not going to disappear due to AI.

Still family-run, there may come a time when the Smith family no longer have an interest in the business, but that doesn’t appear to be the case right now.

The company’s enterprise value of $150 million is about 9.6 times the latest 12-month EBIT (earnings before interest and taxes). That’s the lowest multiple since 2017 and 2010 before that. By comparison, Carlisle’s TEV/EBIT multiple is 15.6x, according to S&P Global Market Intelligence. That’s a big reason Thompson Davis & Co. still own SMID.

The toughest part of owning SMID is the lack of analyst coverage. It’s hard to push a boulder up a hill. However, as recently as Dec. 1, 2024, its shares traded at an all-time high of $51.96. There’s no reason it can’t get back there, given its double-digit sales growth and a never-ending demand for infrastructure.

If you’re patient, you'll make money over the long haul on Smith Midland. That’s a big if for most retail investors.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Airport Chaos Mounts: Is It Time to Sell These 2 Airline Stocks?

- What Options Data Says Could Come Next for GME Stock After GameStop Reports Earnings Tonight

- 2 Reasons Why Western Digital Stock Could Keep Climbing In 2026

- Investors are Piling into Microsoft Call Options - Unusual MSFT Options Activity Today