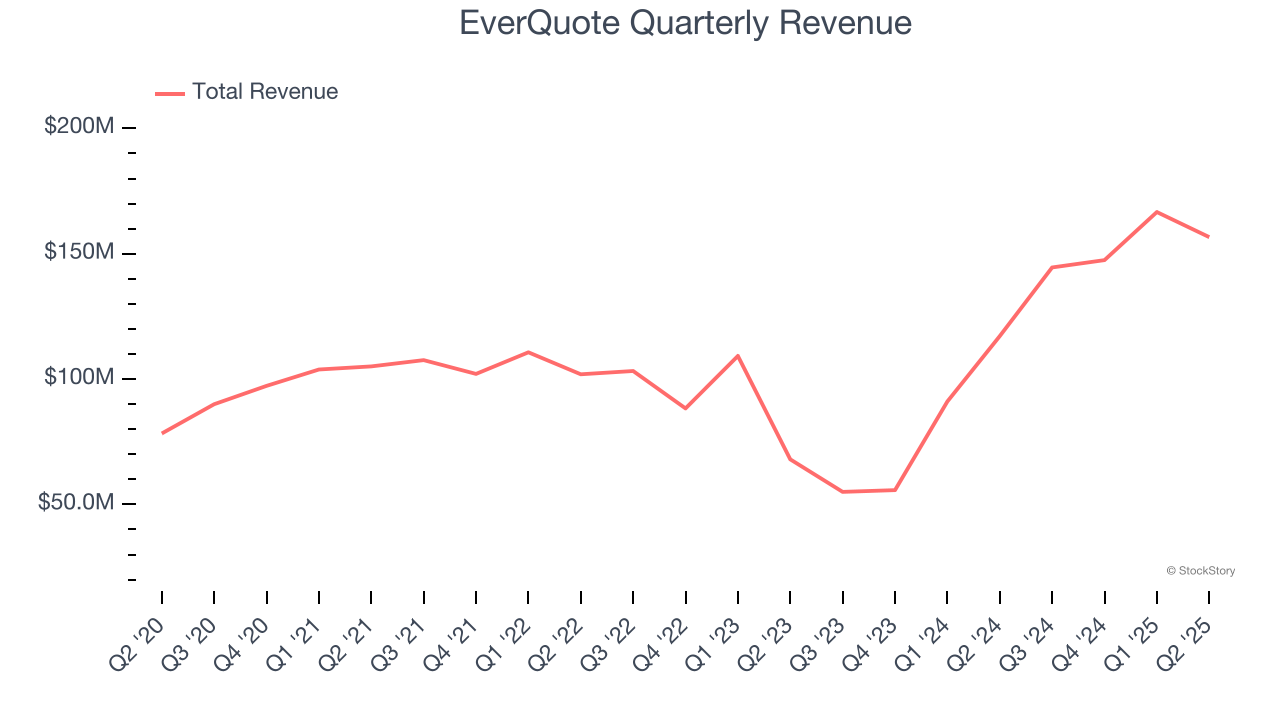

Online insurance comparison site EverQuote (NASDAQ:EVER) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 33.7% year on year to $156.6 million. The company expects next quarter’s revenue to be around $166 million, coming in 0.9% above analysts’ estimates. Its GAAP profit of $0.39 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy EverQuote? Find out by accessing our full research report, it’s free.

EverQuote (EVER) Q2 CY2025 Highlights:

- Revenue: $156.6 million vs analyst estimates of $156.9 million (33.7% year-on-year growth, in line)

- EPS (GAAP): $0.39 vs analyst estimates of $0.35 (9.9% beat)

- Adjusted EBITDA: $21.96 million vs analyst estimates of $21.09 million (14% margin, 4.1% beat)

- Revenue Guidance for Q3 CY2025 is $166 million at the midpoint, above analyst estimates of $164.6 million

- EBITDA guidance for Q3 CY2025 is $23 million at the midpoint, above analyst estimates of $21.17 million

- Operating Margin: 9%, up from 5.4% in the same quarter last year

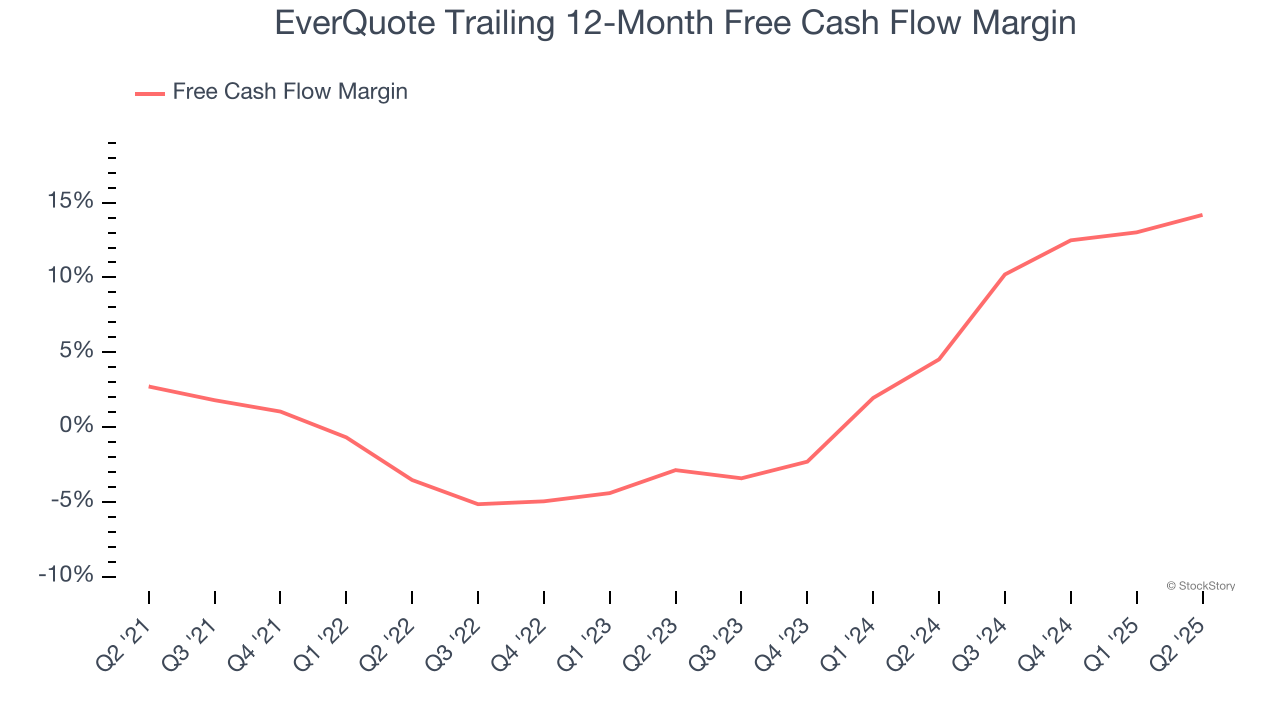

- Free Cash Flow Margin: 15.2%, up from 13.3% in the previous quarter

- Market Capitalization: $871.4 million

“We achieved strong results in the second quarter, growing revenue 34% year-over-year and achieving record operating cash flow,” said Jayme Mendal, CEO of EverQuote.

Company Overview

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, EverQuote’s 13.4% annualized revenue growth over the last three years was decent. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, EverQuote’s year-on-year revenue growth of 33.7% was wonderful, and its $156.6 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 14.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.4% over the next 12 months, a slight deceleration versus the last three years. Despite the slowdown, this projection is above average for the sector and suggests the market is forecasting some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

EverQuote has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.9% over the last two years, better than the broader consumer internet sector.

Taking a step back, we can see that EverQuote’s margin expanded by 17.7 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

EverQuote’s free cash flow clocked in at $23.84 million in Q2, equivalent to a 15.2% margin. This result was good as its margin was 5.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from EverQuote’s Q2 Results

We were impressed by EverQuote’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue was in line. Overall, we think this was a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 10.8% to $22.98 immediately following the results.

So should you invest in EverQuote right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.