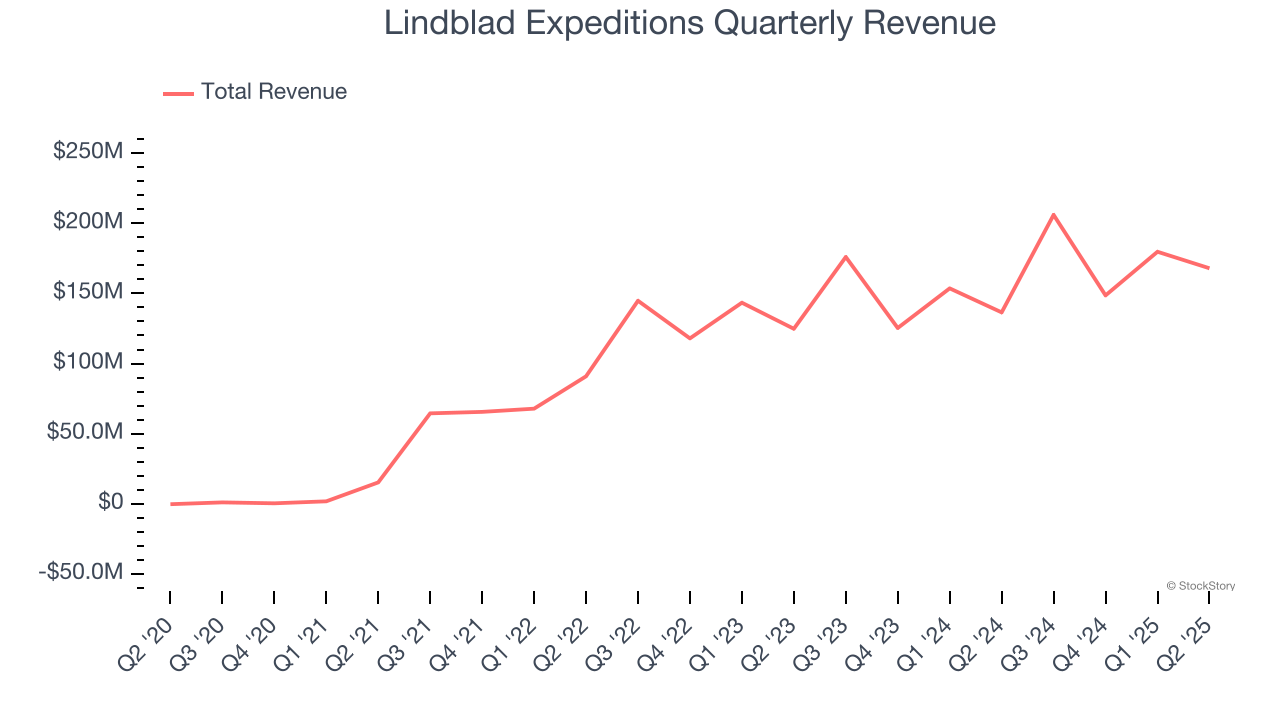

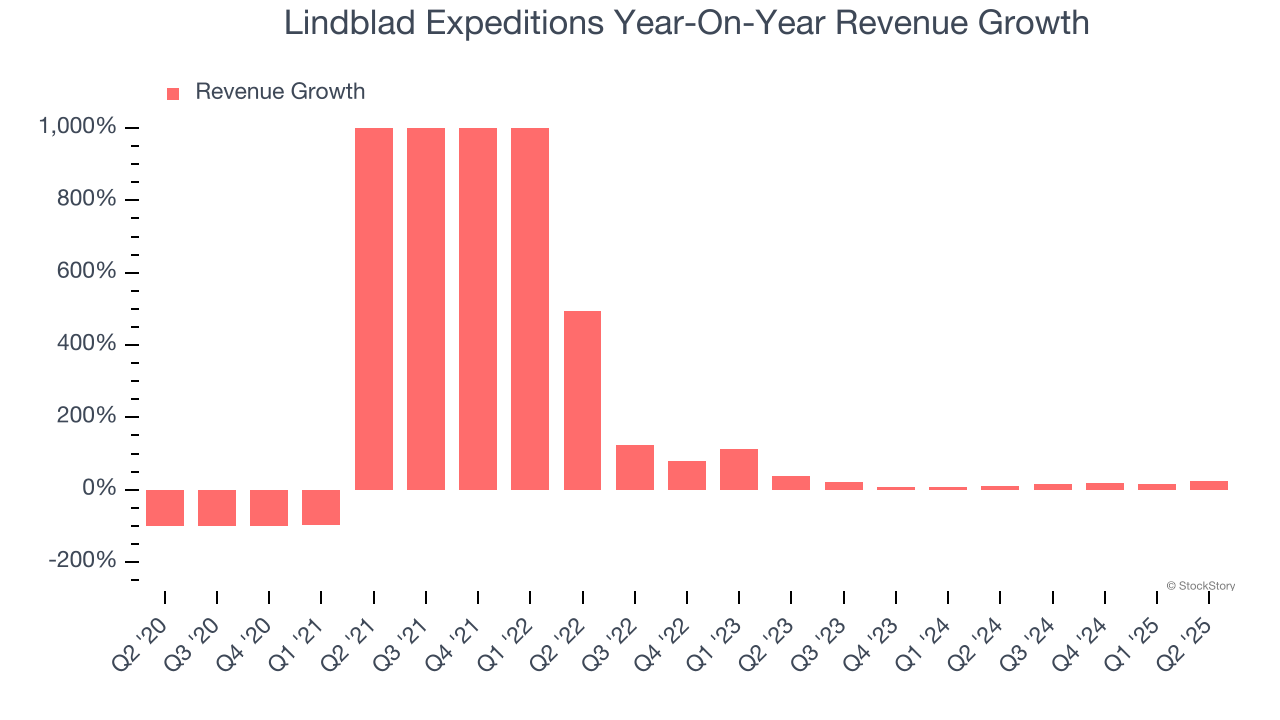

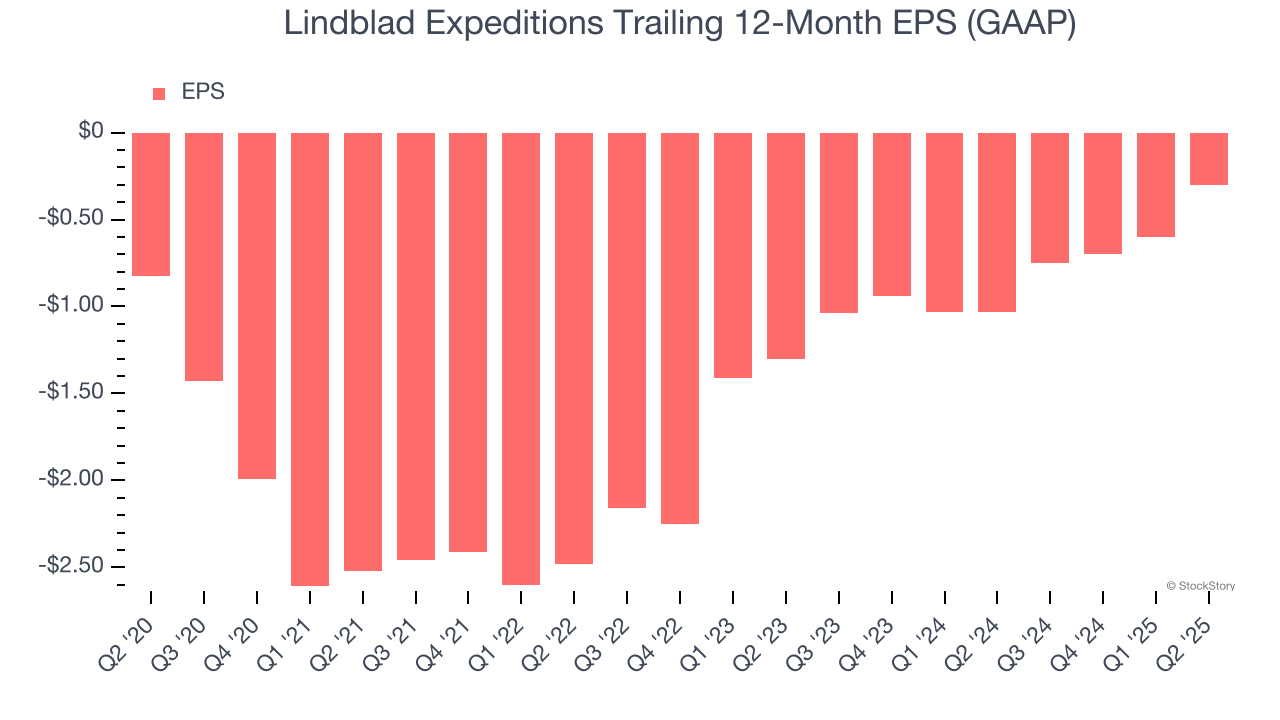

Cruise and exploration company Lindblad Expeditions (NASDAQ:LIND) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 23% year on year to $167.9 million. The company expects the full year’s revenue to be around $737.5 million, close to analysts’ estimates. Its GAAP loss of $0.18 per share was 21.7% above analysts’ consensus estimates.

Is now the time to buy Lindblad Expeditions? Find out by accessing our full research report, it’s free.

Lindblad Expeditions (LIND) Q2 CY2025 Highlights:

- Revenue: $167.9 million vs analyst estimates of $159 million (23% year-on-year growth, 5.6% beat)

- EPS (GAAP): -$0.18 vs analyst estimates of -$0.23 (21.7% beat)

- Adjusted EBITDA: $24.84 million vs analyst estimates of $12.48 million (14.8% margin, 99% beat)

- The company lifted its revenue guidance for the full year to $737.5 million at the midpoint from $725 million, a 1.7% increase

- EBITDA guidance for the full year is $111.5 million at the midpoint, above analyst estimates of $107.6 million

- Operating Margin: 2.6%, up from -6% in the same quarter last year

- Free Cash Flow Margin: 8%, similar to the same quarter last year

- Market Capitalization: $641.7 million

Natalya Leahy, Chief Executive Officer, said "I'm incredibly proud of the team's accomplishments this quarter. We delivered 23% revenue growth, achieved 86% occupancy on a 5% increase in capacity, and drove a 139% increase in Adjusted EBITDA. These results reflect strong momentum behind our strategic initiatives. We remain focused on unlocking meaningful value through continued revenue growth and disciplined cost innovation, and we are confident in the direction we're heading."

Company Overview

Founded by explorer Sven-Olof Lindblad in 1979, Lindblad Expeditions (NASDAQ:LIND) offers cruising experiences to remote destinations in partnership with National Geographic.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Lindblad Expeditions’s sales grew at an impressive 22.2% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Lindblad Expeditions’s annualized revenue growth of 15% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Lindblad Expeditions reported robust year-on-year revenue growth of 23%, and its $167.9 million of revenue topped Wall Street estimates by 5.6%.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Lindblad Expeditions’s operating margin has been trending up over the last 12 months and averaged 3.8% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

This quarter, Lindblad Expeditions generated an operating margin profit margin of 2.6%, up 8.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Lindblad Expeditions’s full-year earnings are still negative, it reduced its losses and improved its EPS by 18.3% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q2, Lindblad Expeditions reported EPS at negative $0.18, up from negative $0.48 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Lindblad Expeditions’s full-year EPS of negative $0.30 will reach break even.

Key Takeaways from Lindblad Expeditions’s Q2 Results

We were impressed by how significantly Lindblad Expeditions blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was in line. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 8.3% to $12.72 immediately after reporting.

Indeed, Lindblad Expeditions had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.